Shipping Markets Adjust to Persistent Route Risks as Tanker Orders Surge and Dry-Bulk Trade Holds Firm

May 2026 | Global Shipping & Freight Markets Desk

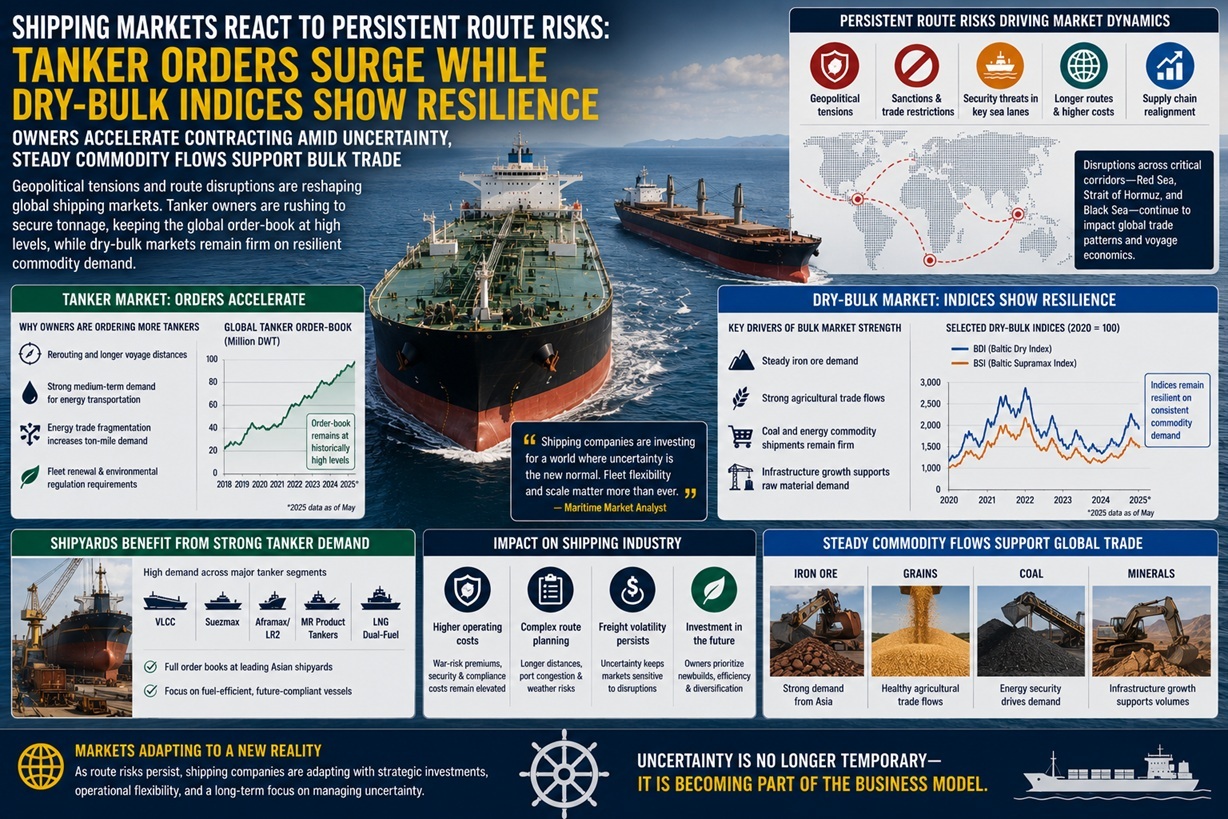

Global shipping markets are increasingly reshaping themselves around persistent geopolitical and trade-route risks, with shipowners accelerating tanker contracting activity while dry-bulk markets continue to demonstrate resilience amid steady global commodity demand.

The diverging trends across vessel segments reflect how the maritime industry is adapting to a world where operational uncertainty, rerouting pressures, and supply-chain security concerns are becoming structural rather than temporary challenges.

Tanker Contracting Accelerates Amid Strategic Uncertainty

Shipowners are continuing to place significant new tanker orders despite heightened geopolitical tension and volatile freight conditions, keeping the global tanker order-book at elevated levels.

Industry analysts attribute the surge in contracting to several factors:

- Persistent rerouting of crude and product cargoes

- Longer voyage distances caused by geopolitical disruptions

- Strong medium-term demand expectations for energy transportation

- Fleet renewal requirements linked to environmental regulations

As sanctions, regional conflict, and security risks reshape traditional trade flows, tanker operators are increasingly seeking fleet flexibility and additional tonnage capacity.

Route Disruptions Driving Structural Demand

The shipping industry has spent much of the past year adjusting to:

- Tensions in the Strait of Hormuz

- Red Sea and Gulf security risks

- Sanctions-related cargo realignment

- Longer alternative routing patterns around high-risk regions

These disruptions have effectively increased “ton-mile demand” — the total distance cargoes must travel — supporting tanker utilization even during periods of broader economic uncertainty.

Owners appear to be betting that:

- Energy trade fragmentation will persist

- Strategic stockpiling will remain elevated

- Long-haul crude transportation demand will stay strong

Shipyards Continue Benefiting From Tanker Demand

Major Asian shipyards are reportedly maintaining strong order pipelines, particularly for:

- VLCCs (Very Large Crude Carriers)

- Suezmax tankers

- Product tankers

- LNG dual-fuel designs

The sustained contracting pace is helping keep global order-books at historically high levels despite concerns over:

- Inflationary pressure

- Financing costs

- Slower global economic growth

Shipbuilders are also benefiting from owners seeking newer, more fuel-efficient vessels capable of meeting tightening emissions standards.

Dry-Bulk Sector Shows Unexpected Resilience

While tanker markets are driven by geopolitical dynamics, the dry-bulk sector is being supported by relatively stable commodity trade flows.

Bulk freight markets continue to benefit from:

- Steady iron ore demand

- Agricultural trade movements

- Coal and energy commodity shipments

- Infrastructure-related raw material demand in emerging markets

Despite periodic volatility, dry-bulk indices have remained comparatively resilient, reflecting ongoing industrial and commodity consumption across major economies.

Commodity Demand Offsetting Broader Economic Concerns

Shipping economists note that dry-bulk resilience is particularly notable given:

- Slower global GDP growth

- Persistent inflation in several economies

- Trade uncertainty linked to geopolitical fragmentation

Strong underlying commodity demand, especially across Asia, has helped offset weaker sentiment in other sectors of the global economy.

For operators, this has translated into:

- More stable charter activity

- Improved vessel utilization

- Reduced downside pressure on freight earnings

Insurance, Compliance, and Operating Costs Remain Elevated

Across both tanker and bulk segments, shipowners continue to face higher operating complexity due to:

- War-risk insurance premiums

- Security compliance measures

- Route planning challenges

- Emissions and environmental regulations

These factors are increasingly influencing:

- Fleet investment decisions

- Chartering strategies

- Vessel deployment patterns

- Long-term contracting behavior

Industry Outlook: Adaptation Becoming Permanent

Market observers believe the maritime industry is transitioning into a new operational era where:

- Geopolitical disruption becomes a long-term planning factor

- Supply chains remain more regionally fragmented

- Fleet flexibility gains strategic importance

- Freight volatility becomes structurally embedded in markets

Rather than waiting for stability to return, shipping companies are now actively investing around continued uncertainty.

The Bottom Line

Global shipping markets are no longer reacting to isolated disruptions, they are adapting to a permanently more complex operating environment.

As tanker owners accelerate fleet expansion amid persistent route risks and dry-bulk markets remain supported by resilient commodity demand, the maritime industry is demonstrating an important shift:

uncertainty is no longer temporary, it is becoming part of the business model.